The tokenization of real-world property has provided promise and frustration in equal measure, however one blockchain platform claims regulation is the important thing to success.

Whereas TradFi incumbents applaud their potential for extra environment friendly settlements, others argue tokenization is over-hyped and negates crypto’s decentralization premise. Swarm, a fully-regulated decentralized platform that tokenizes real-world property to be used in decentralized finance, begs to vary.

In an interview with BE[IN]CRYPTO, co-founders Philipp Pieper and Timo Lehes argue regulation is the important thing, not the enemy, to preserving the fame of the blockchain sector after the failure of FTX. Does Swarm have the reply to the way forward for crypto within the US?

We discover the reply right here. However first, we’d like a short intro tokenization, the engine powering Swarm’s optimism.

A Temporary Historical past of Tokenization and the Rise of NFTs

Digital tokenization began within the 2000s to guard delicate knowledge from unauthorized use. Primarily, a 3rd occasion would obtain affirmation of delicate data with out being granted direct entry.

Tokenization course of in e-commerce | Supply: Ebanx

Earlier than that, within the eighteenth century, the US authorities secured or tokenized {dollars} with bodily gold till 1971. Later, the fiat system issued banknotes backed by the complete religion of the US authorities.

At this time, corporations wishing to guard delicate knowledge retailer tokens on the cloud. Cost corporations like Mastercard grant third-party entry to buyer knowledge by means of the change of tokens.

Nonetheless, the arrival of the Ethereum blockchain in 2015 and its tokenization requirements have since reworked the rights tokens bestow on house owners. Non-fungible tokens, or NFTs, grant holders immutable custody of digital or bodily property.

On most chains, an asset proprietor tokenizes their property by means of a particular course of referred to as “minting.” NFTs on Ethereum should conform to its Request for Remark-721 token guidelines.

Within the minting course of, the creator should embrace bits of knowledge within the NFT, corresponding to the principle content material that will probably be unlocked when a purchaser takes possession. For instance, within the case of a Bored Ape Yacht Membership NFT, the principle content material is a 2D drawing of a cartoon ape.

The NFT may additionally include perks that creators use to extend the token’s worth. Extras can embrace entry to on-line boards and bodily occasions.

Till now, most main firms have struggled to understand the complete enterprise potential of NFT perks. Gucci, Chipotle, Nike, and Starbucks are among the many few to have realized the potential of tokenization in rewarding loyal prospects.

Banks Lead Business Purposes of Tokenization

However conventional finance companies, weighed down by legacy networks, have lengthy been testing the expertise’s skill to settle transactions shortly.

Citigroup tokenized a proprietary asset, Citicoin, on its non-public community in 2015. It later tapped Swiss crypto firm Metaco to carry prospects’ digital property.

JPMorgan’s JPM Coin tokenized {dollars} for consumer funds on a customized chain in 2019. It just lately tokenized euros with JPM Coin, with German Conglomerate Siemens AG performing the primary transaction.

Funding financial institution Goldman Sachs stated in November final 12 months its blockchain efforts would deal with tokenization and the rewiring of economic markets. Later that 12 months, Singapore’s central financial institution examined tokenized fiat forex transfers by means of a blockchain asset pool.

In July, South Korea’s oldest financial institution confirmed its testing of remittances with a number of tokenized Southeast Asian currencies.

Swarm Says Tokenization is the Path to Regulated DeFi

However can tokenization transfer past legacy banking? Sure, says Swarm, a fully-regulated platform linking the protection of TradFi regulation with the liberty of decentralized finance (DeFi).

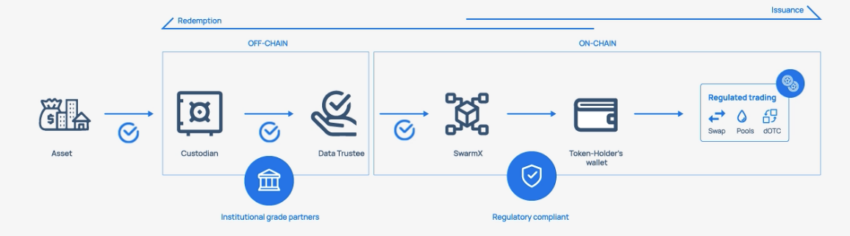

Swarm opens DeFi entry to tokenized bonds and securities backed by regulation. It retains buyer property with an establishment like Gemini or Coinbase, which defend keys giving entry to digital tokens.

How a buyer withdraws tokenized asset | Supply: Swarm

A “withdrawal” pulls the asset from the custodian by means of a digital trustee onto Swarm’s community. From there, the asset is transferred to a buyer pockets to be used in DeFi.

Considering how DeFi protocols use property as collateral? Learn extra right here.

Swarm’s bosses argue the correct mix of regulation and decentralization is essential to the survival of the crypto sector after the failure of FTX. They argue,

“The requirements for bringing property on-chain have to be rigorous, and the onus is on these within the tokenization house to get this proper. Failing to take action will end in a lack of confidence within the blockchain sector.”

Swarm has secured a license to commerce tokenized property with the German finance company BaFin. Whereas the method required compliance with anti-money laundering and capital laws, the pair argues their enterprise later “felt very very similar to DeFi.”

“Being one of many first BaFIN-regulated DeFi corporations was no stroll within the park. It is because DeFi will not be a pure match for the regulatory fashions of conventional finance.

They favored the very fact transactions are on-chain, that means they’ll look beneath the hood themselves to see what’s going on, slightly than relying solely on a report we generate ourselves months down the road.”

The BaFin license additionally means Swarm received’t want new vetting when Europe’s Markets in Crypto-Property invoice goes into impact in 2024.

The founders declare Swarm is the primary decentralized platform to supply regulated buying and selling of tokenized property. The corporate gives tokenized shares of publicly traded US corporations, together with BlackRock, Coinbase, Nvidia, and Microsoft.

Liquidations in DeFi Purposes Problem Swarm Tokenization Promise

It stays to be seen whether or not tokenized property will upend DeFi markets as Swarm hopes. A number of latest exploits have revealed the fragility of the business and its want for higher code audits.

Notably, Swarm didn’t focus on the implications of dropping a digital asset locked in a borrowing good contract.

Moreover, the founders didn’t element how Swarm would course of liquidations if DeFi loans grew to become undercollateralized. DeFi gamers may additionally be uncomfortable leaving their costliest property weak to theft.

At present, few international locations’ legal guidelines totally tackle DeFi dangers. Earlier this 12 months, the US SEC stated it might crack down on DeFi companies breaking present US change guidelines.

MiCA will seemingly sort out the problem when revised, whereas a brand new DeFi US invoice awaits Congressional passage. The invoice imposes cash laundering checks on DeFi apps.