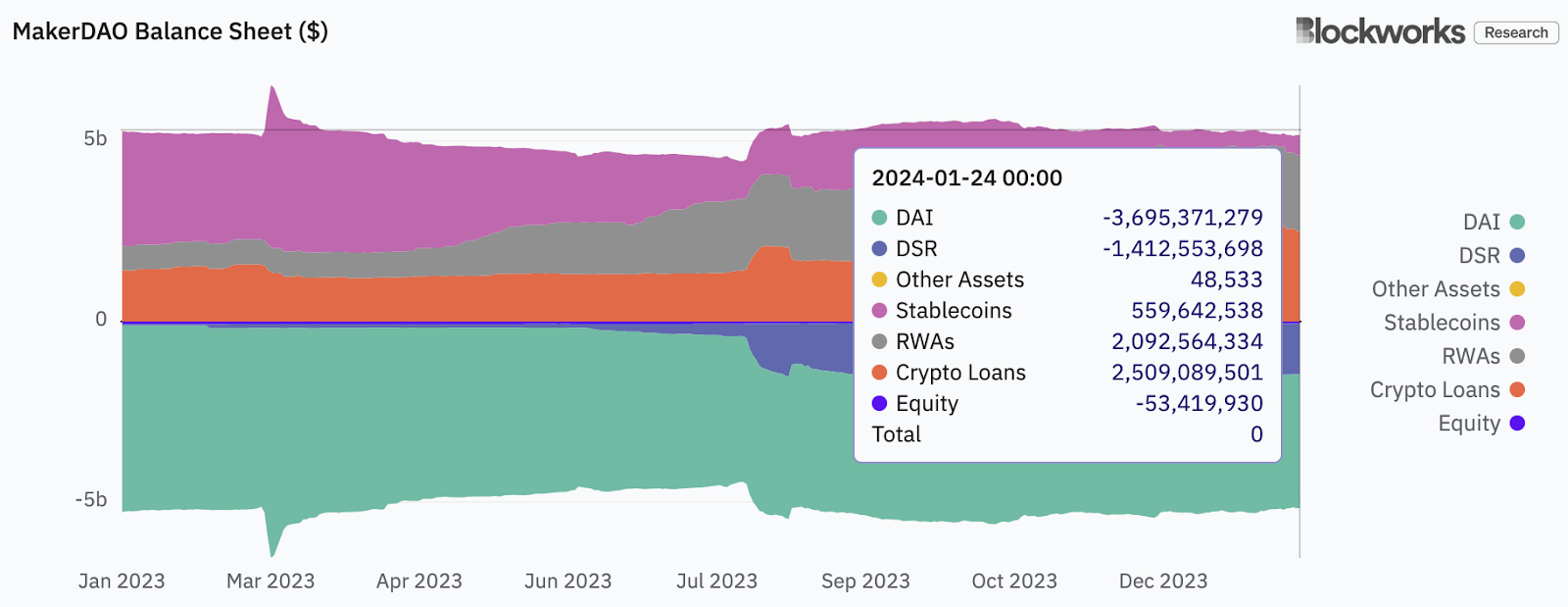

MakerDAO, issuer of the DAI stablecoin, has seen a notable shift within the composition of its stability sheet because of the mixture of macroeconomic occasions and surging crypto markets.

The newest information from the DAO’s Digital Asset-Legal responsibility Committee (ALCO) exhibits that crypto-backed loans — that’s, DAI issued in opposition to crypto collateral like ether — as soon as once more signify greater than 50% of whole belongings, for the primary time since Could 2022.

For many of 2023, Maker’s public credit score portfolio — assume US T-bills — dominated the protocol’s income, as Federal Reserve fee hikes pushed rates of interest on quick time period Treasurys above 5%.

However as yields fell within the fourth quarter of the 12 months and demand for DAI borrowing picked up, the DAO, by its Particular Goal Automobile (SPV) intermediaries started to unload T-bills, in line with Sebastian Derivaux at Steakhouse Monetary, which advises the DAO.

“The rationale we’re reducing T-bill publicity to replenish the [Peg Stability Module] and the explanation why the PSM is shrinking currently is as a result of we’re in a bull market,” Derivaux advised Blockworks. “And in order you may see, the crypto financial institution loans are going up quite a bit as a result of individuals wish to be speculating, and each time somebody takes a mortgage [from] MakerDAO to get leverage, it decreases the PSM by the identical quantity, roughly.”

Learn extra: MakerDAO could develop non-crypto asset portfolio with BlockTower, Centrifuge

The ALCO flagged one merchandise of delicate concern associated to the provision of stablecoins in Maker’s PSM within the minutes from its most up-to-date assembly, revealed Wednesday.

“Day by day liquidity has been persistently a bit quick over the previous few months,” the committee wrote. “The Digital ALCO recommends a medium-term precedence to shift liquidity again a bit.”

The DAO has a goal to have a minimum of 18% to 22% of stablecoins accessible for the PSM, in line with Derivaux.

“So generally it goes a bit down after which one thing is completed to replenish the PSM,” he mentioned.

Recently, the ratio of stablecoins to whole belongings has been operating nearer to 10%-12% in line with Blockworks Analysis information.

ALCO mentioned diversifying the protocol’s stability sheet additional, particularly analyzing the suitability of Collateralized Mortgage Obligations (CLOs) and different asset courses as potential additions to hunt greater yield than T-bills.

The committee acknowledged that it might be needed to increase the length of investments barely, whereas being aware of the chance related to a possible return to a low rate of interest macro setting down the highway. CLOs usually have variable charges.

Learn extra: MakerDAO strikes $250M from Coinbase to rebuild DAI collateral

For belongings paying greater than T-bills, the committee thought-about senior tranches of Asset Backed Securities (ABS), particularly these underpinned by floating belongings like bank card receivables in addition to short-term ETF bond funds.

These could juice returns whereas leaking threat low, however with tradeoffs, in addition to potential challenges integrating these belongings into Maker’s algorithmic Asset-Legal responsibility Administration (ALM) scheme.

The ALCO not too long ago added conventional finance heavyweight Moorad Choudhry as an unbiased advisor.

Steakhouse has primarily based parts of its ALM analysis and proposals on Choudhry’s work in academia as a professor within the Division of Economics at London Metropolitan College and writer of textbooks and references on finance.

Whereas the ALCO concluded that holding extra asset varieties might assist develop the stability sheet by rising the Dai Financial savings Charge (DSR) — which is presently at 5% — it emphasised the necessity for cautious consideration of capital adequacy, liquidity, worth transparency and threat administration integration.

Learn extra: DAI Financial savings Charge is at 8%, simply not for Individuals

A excessive proportion of the DAI that has been minted isn’t being staked for the 5% yield. Derivaux mentioned that as a lot as 70% is simply sitting in Externally Owned Accounts (EOAs) on Ethereum or layer-2 chains.

“That’s fairly stunning as a result of sDAI — perhaps it’s not identified by individuals — but it surely’s utterly riskless,” he mentioned, referring to the chance relative to holding unstaked DAI, which yields nothing.

The 5% fee must be sustainable, Derivaux mentioned, because the stability sheet composition shifts. Demand for leverage ought to make collateral backed loans extra worthwhile for the protocol.

“Clearly the much less stablecoins we have now [on the balance sheet], the extra income MakerDAO is producing and the extra revenue it’s producing,” he famous.